Electrical Distribution Systems & The Hidden Wiring in Your Depreciation Strategy

Every real estate investor knows that buildings depreciate over decades while equipment writes off much faster. But few realize that the electrical infrastructure hidden behind walls, above ceilings, and inside mechanical rooms can (and often should) follow the same split. That junction box, that conduit run, that dedicated breaker: is it part of your 39-year building, or is it an appendage of your 5-year equipment? Answering that question correctly can unlock substantial tax deferral without inventing a single deduction. And the answer hinges not on guesswork, but on an engineering-driven, functionally-rooted analysis that aligns with the IRS Cost Segregation Audit Techniques Guide (ATG).

This post distills the key principles every investor and CPA needs to understand about electrical distribution systems (EDS) in cost segregation. You’ll walk away knowing how EDS classification separates building power from equipment power, how functional allocation transforms electrical costs into defensible shorter-life assets, which property types stand to benefit most, and why upfront documentation makes the difference between a study that holds up and one that collapses under review. Let’s pull back the panel cover.

§1250 Building Power vs. §1245 Equipment Power

A building’s electrical distribution system is not a monolithic asset. It’s a layered network: service entrance, transformers, main switchgear, distribution panels, subpanels, feeder wiring, branch circuits, disconnects, and dedicated outlets. For tax purposes, the IRS does not treat these components uniformly. The classification rests on what each segment serves.

The IRS Cost Segregation ATG draws a clear line: electrical distribution that is “directly associated with specific personal property” and “necessary for the operation of such property” can qualify as §1245 personal property, typically depreciable over 5 or 7 years. Meanwhile, electrical infrastructure that powers general building operation (lighting, HVAC, general-use receptacles, life safety systems, etc.) remains §1250 real property, recovering over 39 years (nonresidential) or 27.5 years (residential rental).

This is not a judgment call about how “important” a circuit is. It’s a functional test. A dedicated 480V disconnect serving a commercial oven serves a piece of equipment, not the building envelope. A 120V convenience outlet in a breakroom serves the building. The distinction is embedded in design drawings, panel schedules, and load calculations. Ignore it, and you’re likely over-depreciating some assets while under-depreciating others.

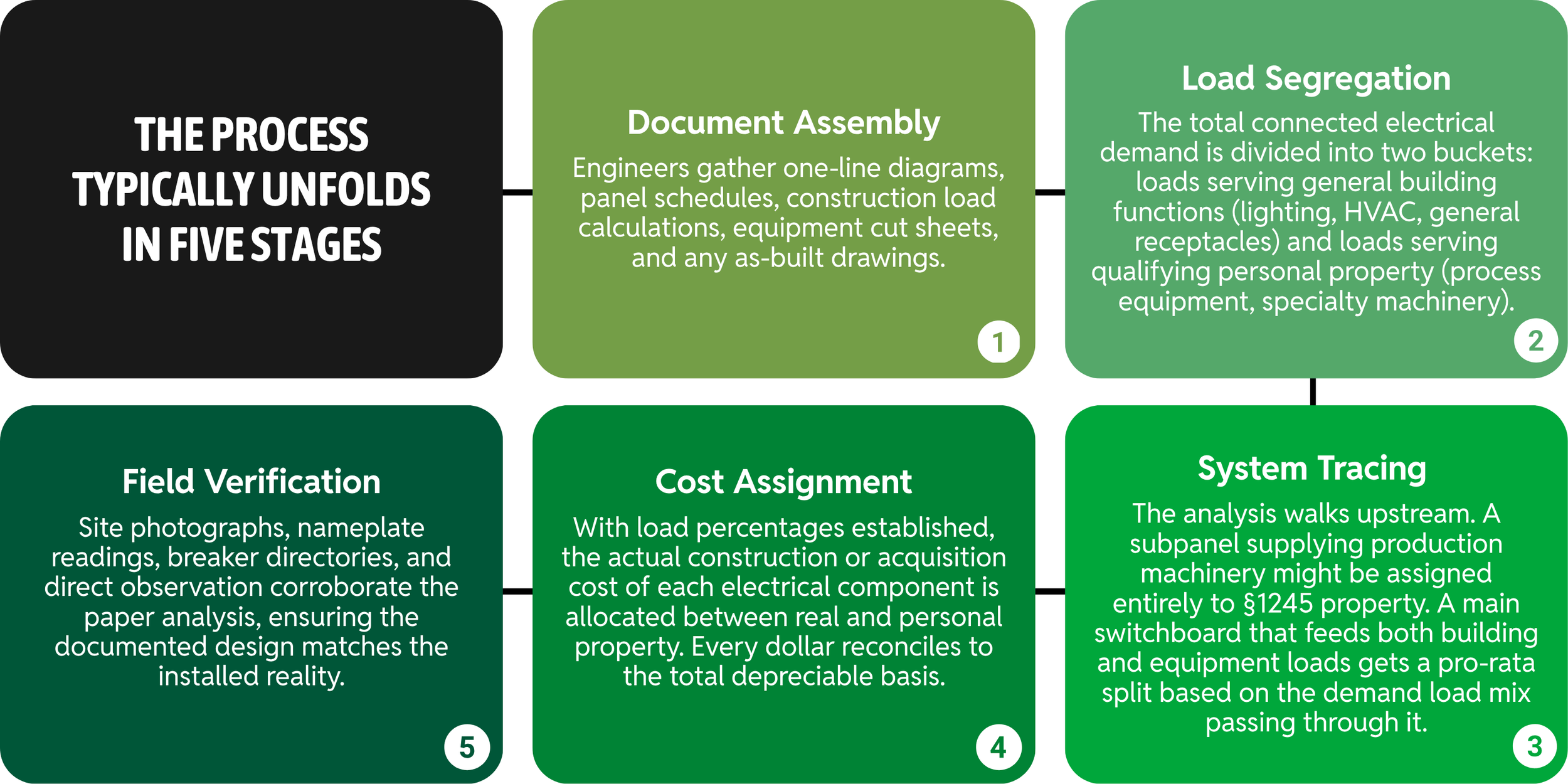

How Functional Allocation Transforms Engineering Data into Tax Classification

Functional allocation is the disciplined alternative to the all-too-common “percentage of electrical” shortcut. It works by tracing the actual power demand from end-use equipment back through the distribution hierarchy, allocating electrical infrastructure costs proportionally based on what the loads serve.

This methodology mirrors the “detailed engineering approach” endorsed by the IRS ATG. It replaces broad assumptions with verifiable data, giving the CPA who signs the return a clear audit trail from tax classification back to the building’s physical infrastructure.

Where EDS Analysis Delivers the Greatest Impact

Not every building contains a goldmine of reclassifiable electrical costs. EDS analysis yields its strongest returns when a property houses significant electrical loads dedicated to business or production equipment. Common high-opportunity categories include:

Grocery Stores and Supermarkets: Refrigeration systems, compressors, display cases, deli and bakery equipment, and point-of-sale terminals all demand dedicated circuits and disconnects.

Restaurants: Commercial kitchens brim with equipment requiring specialized electrical connections like ovens, fryers, walk-in coolers, dishwashers, and exhaust hoods.

Medical and Dental Offices: Imaging equipment (MRI, CT, X-ray), sterilization units, and lab analyzers frequently require dedicated power drops and isolated panels.

Manufacturing and Industrial Facilities: Process machinery, CNC tools, conveyor systems, and testing stations almost always rely on dedicated electrical infrastructure that is entirely separable from general building power.

Cold Storage and Warehousing: Large-scale refrigeration units, blast freezers, and automated material handling systems drive substantial electrical demand that can be directly traced.

Residential rental properties present a more fact-specific picture. A dedicated 50-amp range circuit or an electric vehicle charger may support personal property, but general-purpose circuits throughout living spaces typically do not. The same functional test applies, even if the dollar amounts are smaller.

What matters across all property types is that the analysis is driven by actual load data, not by a generic assumption that “X percent of electrical costs” qualifies.

Act Before the Study Begins

A cost segregation study is only as strong as the records that feed it. Investors who gather electrical documentation early (ideally during construction, renovation, or immediately after acquisition) give their engineering team the best possible foundation.

For new builds and major renovations, retain:

Electrical one-line diagrams and panel schedules

Load calculations stamped by the design engineer

Detailed contractor cost breakdowns that itemize electrical work by system or area

Photographs of conduit runs, dedicated disconnects, and panel interiors during construction

For acquired existing properties, request as-built drawings, prior tenant improvement records, and equipment specifications from the seller. When documentation is thin, the site inspection becomes paramount. Experienced engineers photograph nameplates, breaker schedules, and dedicated receptacles, building the evidence file from scratch.

Timing matters too. Coordinating the study while contractors, architects, and facility managers are still accessible often yields cleaner data than chasing records months after a project closes out. A well-documented EDS allocation increases short-life percentages and makes the entire study more resilient under IRS review.

The USTAGI Approach

At US Tax Advisors Group, Inc., we treat electrical distribution systems as a technical exercise, not a guessing game. Our studies are built on a foundation of licensed engineering analysis, on-site inspection, and meticulous reconciliation to the IRS Cost Segregation ATG. We don’t apply flat percentages. We read panel schedules. We trace feeders. We separate building power from equipment power because that’s what the tax law and your cash flow demands.

Whether you’re acquiring a grocery-anchored retail center, building out a restaurant, or expanding a manufacturing facility, a defensible EDS analysis can put more depreciation to work in the years it matters most. Ready to uncover what’s hiding behind your panels? Contact USTAGI today to discuss your property and request a preliminary benefit estimate or a full cost segregation study. Our team partners with investors and CPAs to ensure every electrical component is classified correctly, every deduction is fully supported, and your study stands up to scrutiny.

Let’s power your depreciation strategy with the right engineering.